ADVERTISEMENT

ADVERTISEMENT

Duty Waiver: A Temporary Fix for the Cotton Problem

The long-term solution lies in improving farm productivity through better seed technology, climate-resilient varieties, irrigation efficiency etc.

-

Himanshu Jaiswal

Himanshu Jaiswal - Wed, 17, Jun 2026

- 04:01 EDT

- 32

Cotton / unsplash.com

Cotton / unsplash.com

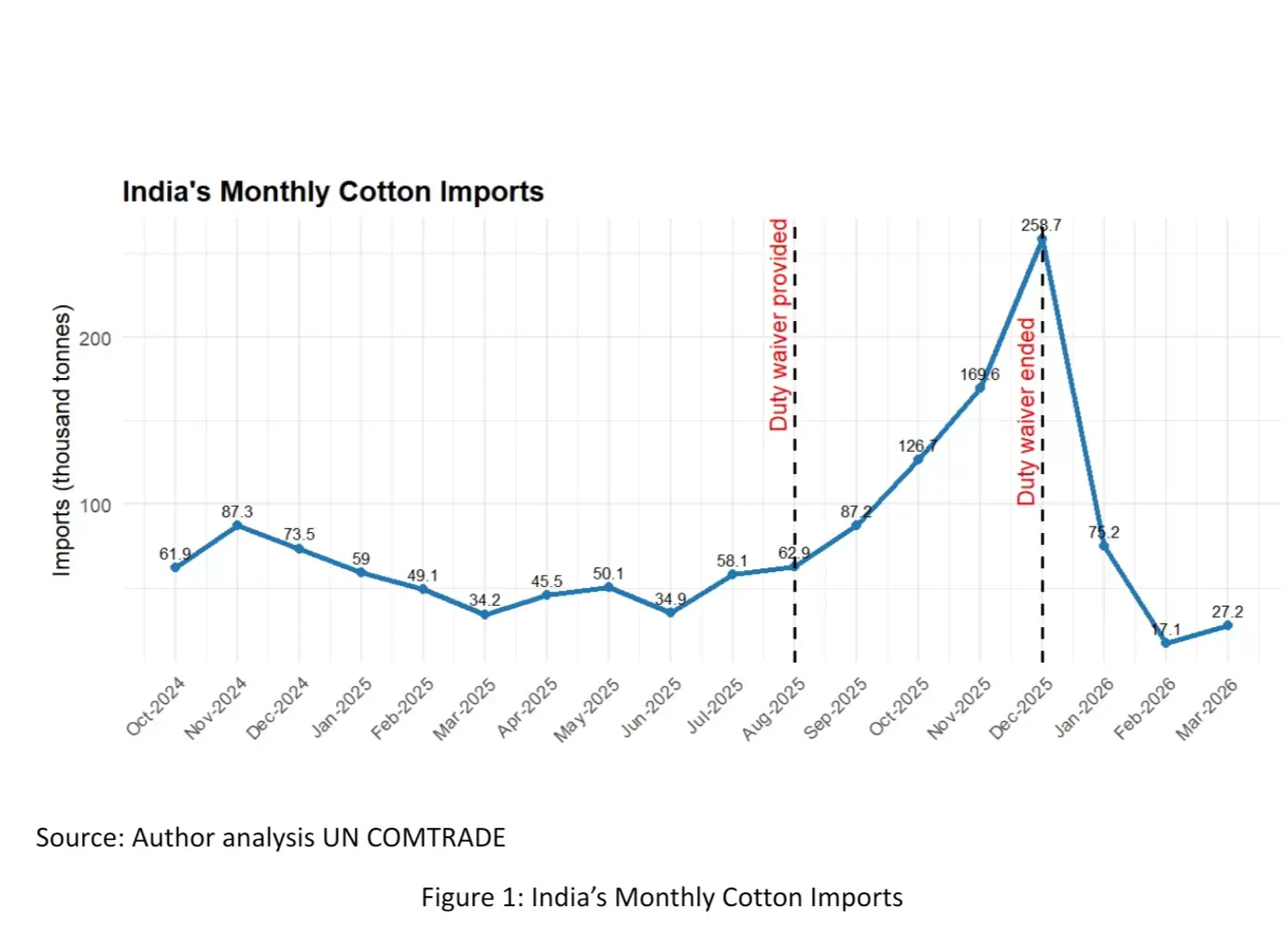

India’s temporary duty waiver on cotton imports between August and December 2025 appears to have provided meaningful short-term relief to the domestic textile industry. As shown in Figure 1, cotton imports remained moderate until mid-2025, but rose sharply after the waiver was introduced in August.

Imports climbed from 62.9 thousand tonnes in August 2025 to a peak of 258.7 thousand tonnes in December 2025, suggesting that importers actively utilised the duty-free window to augment domestic supply. Once the waiver ended in December and import duty of 11.064 per cent was reinstated from January 2026 onward, imports fell sharply to 75.2 thousand tonnes in January 2026, and further to 17.1 thousand tonnes in February, indicating the direct effect of tariff policy on import volumes.

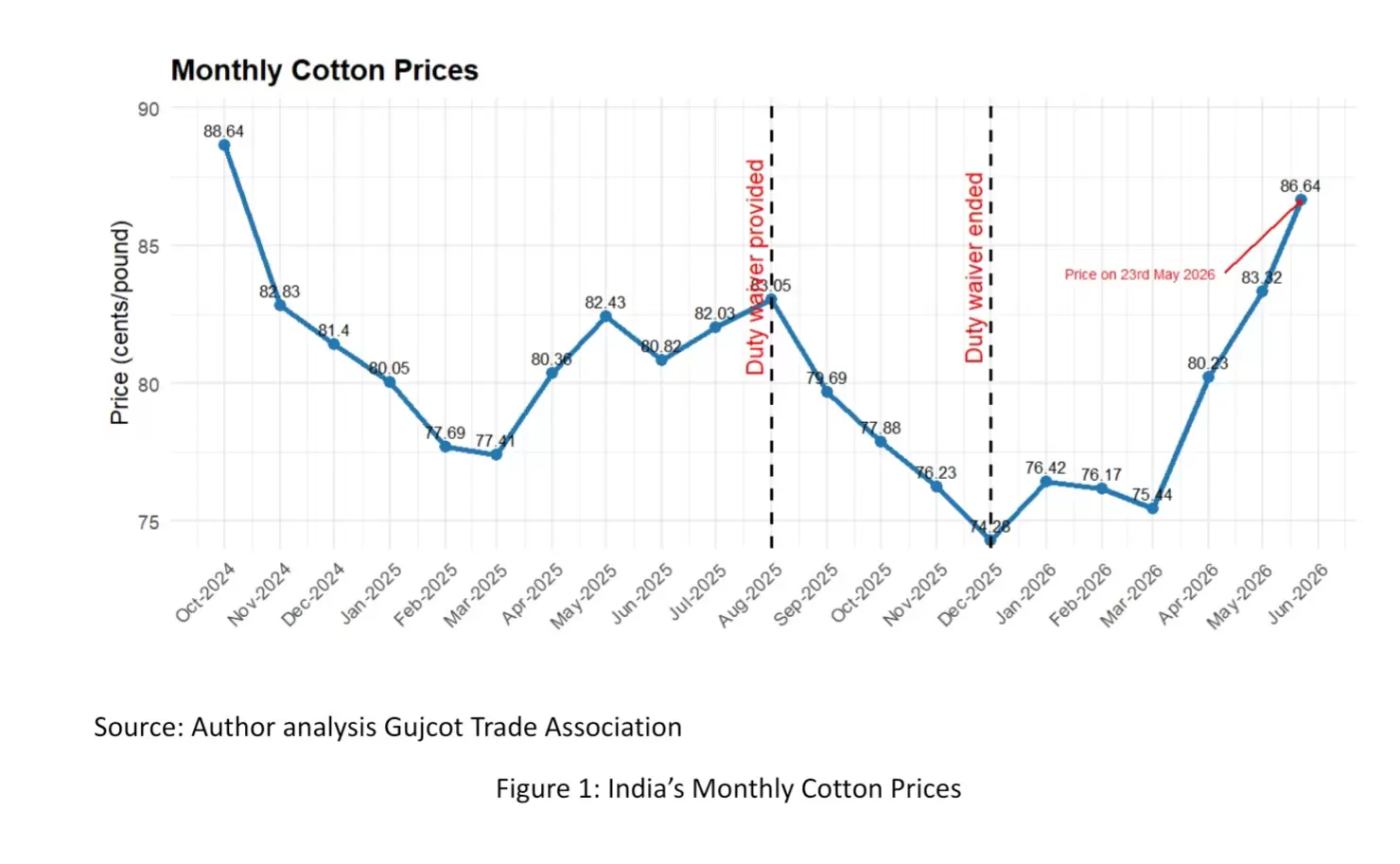

At the same time, Figure 2 shows that domestic cotton prices, tracked through the Shankar-6 benchmark, also softened during the waiver period. Prices, which stood at around 83 cents per pound in August 2025, gradually declined to 74.3 cents per pound by December 2025. This suggests that the increase in imported cotton helped ease supply-side pressure and stabilise prices in the domestic market.

However, after the duty waiver lapsed, prices again began to rise, reaching 86.6 cents per pound by May 2026. Taken together, the import and price trends indicate that the waiver acted as an effective temporary instrument for managing supply tightness and calming market prices.

But tariff waivers are ultimately a short-term response. The structural challenge lies deeper in India’s cotton productivity. Despite being the world’s second-largest producer and consumer of cotton—and accounting for nearly one-fifth of global cotton production and consumption—India’s average cotton yield remains around 440 kg per hectare, significantly below the global average of roughly 840 kg per hectare.

In comparison, China’s yield exceeds 2,000 kg per hectare. This means India produces large volumes largely because of acreage, not productivity. Sustained competitiveness in the cotton-textile value chain will therefore require more than periodic import-duty relief. The long-term solution lies in improving farm productivity through better seed technology, climate-resilient varieties, irrigation efficiency, mechanisation, and stronger agricultural R&D. Without addressing these structural constraints, supply disruptions and price volatility are likely to recur across the cotton value chain, affecting both industry and livelihoods.

Discover more at New India Abroad.

Related

.png)

ADVERTISEMENT

ADVERTISEMENT

E Paper

Video

Comments

Start the conversation

Become a member of New India Abroad to start commenting.

Sign Up Now

Already have an account? Login