ADVERTISEMENT

ADVERTISEMENT

Save the best for last: The changing financial dashboard of Indian savers

The faith of new investors who entered the stock market through mutual funds, SIPs and ETFs , has been put to the test amid volatile markets and uneven returns.

-

Sarika Rachuri

Sarika Rachuri -

Badri Narayanan Gopalakrishnan

Badri Narayanan Gopalakrishnan - Sat, 20, Jun 2026

- 23:44 EDT

- 18

Representative image / File Photo/ Reuters

Representative image / File Photo/ Reuters

In the past two decades, as India has gravitated from a thrift mindset to an abundance mindset, there has been a change not just in our propensity to save, but also in our tendency to look for newer avenues of saving. Generation X, often called the sandwich generation, and the pre-liberalisation kids were products of a thrift economy where saving was a virtue and financial discipline meant putting aside money bit by bit.

The government then, stood at the forefront of this effort and took a moral responsibility for encouraging savings. Going by the Nudge Theory, the savings architecture was built on the bedrock of tax regimes that incentivised saving and rewarded financial discipline.

The thrift mindset was also a structural outcome of an economy that had very few other avenues and options. Unlike the West, where the credit revolution had already taken root, India had limited avenues for borrowing and consumption. The backbone of household savings comprised of what were called “small savings” - Kisan Vikas Patra, NSCs (National Savings Certificates), post office schemes and bank deposits, and provident funds and insurance products. With limited access to capital markets and consumer credit, the Indian middle class channelled a significant proportion of its savings into these government-backed instruments. Small-savings schemes alone accounted for nearly 14 per cent of net household financial savings by the late 1990s.

Several reasons were attributed to this. The government provided huge incentives through tax-saving schemes under various sections of the Income Tax Act. Savings routed through these schemes offered significant relief to taxpayers and encouraged a good culture of forced saving.

Fast forward to recent years, and a disquieting trend that policymakers are grappling with is the decline in household savings. This trend became particularly discernible in the aftermath of the COVID pandemic. Household net financial savings, which stood at around 11.5 % of GDP in FY21, fell sharply to about 5 % in FY23 before recovering modestly thereafter to 6% in FY 24-25. While savings have inched up in recent years, they remain well below their pre-pandemic-era highs.

One discernible trend has been a transformation of the savings dashboard. Capital market reforms, financial inclusion, and rising GDP have brought a significant shift in the savings profile. Indian households are being metamorphosised from savers into investors.

Also Read: NDA hails Narendra Modi as country's longest serving Prime Minister

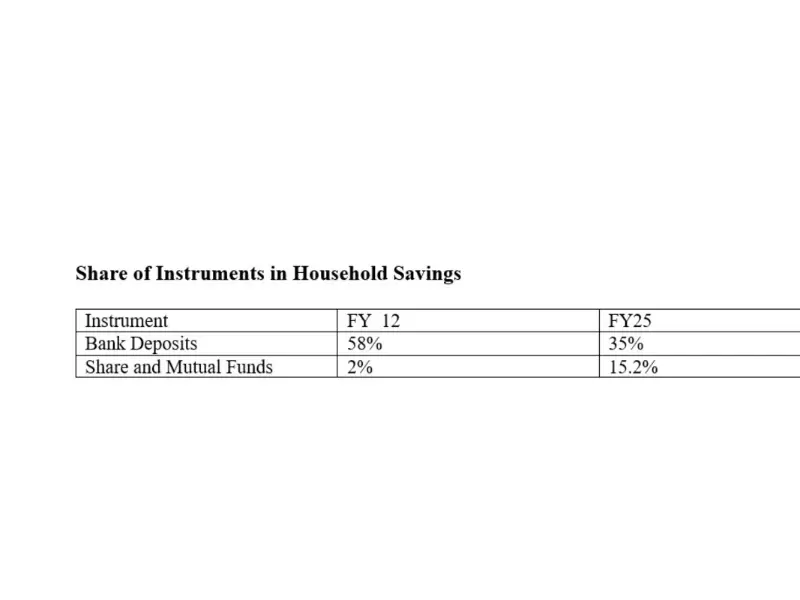

The mutual fund and SIP (Systematic Investments Plan) route, in particular, has enabled the average household investor to participate in capital markets, an avenue that was once largely restricted to a small segment of the population. This can be seen from the table below:

Share of Instruments in Household Savings / Economic Survey 2024-25.

Share of Instruments in Household Savings / Economic Survey 2024-25.In addition, the new tax regime no longer dictates investment choices the way it once did. Earlier, the small savings schemes occupied the centre stage for decades, aided by the tax reliefs they offered. However, the new tax regime has altered the savings landscape, allowing households to make investment decisions that are driven less by tax considerations and more by risk-return preferences.

Consequently, small saving schemes, bank deposits that once were popular choices have lost their dominance The choice of market-linked instruments also corroborates to the demographic profile of Indian households. The median age of India is around 28–29 years. A younger India, entering the workforce and building its financial base, typically exhibits a higher risk appetite and finds market-linked investment options more appealing compared to traditional small savings schemes.

This changing landscape of India brings out a discernible nudge towards market-linked schemes. However, the faith of new investors who entered the stock market through mutual funds, SIPs and ETFs (Exchange Traded Funds), has been put to the test amid volatile markets and uneven returns, in recent times. The earlier generation adopted a disciplined approach towards systematically investing in small-savings schemes. Time alone will tell whether, Gen Z will remain equally steadfast in its commitment to market-linked investments and save their best for last.

Discover more at New India Abroad.

Related

ADVERTISEMENT

ADVERTISEMENT

E Paper

Video

Comments

Start the conversation

Become a member of New India Abroad to start commenting.

Sign Up Now

Already have an account? Login